Markets Remain Resilient Amid Renewed Geopolitical Tensions

WEEKLY MARKET SUMMARY

Global Equities: Markets proved resilient in their first full trading week of the 2026 second half, shrugging off renewed US-Iran hostilities. The Dow Jones Industrial Average set a fresh record close of 53,056 on Monday, topping 53,000 for the first time, but gave back ground as the week wore on and ended -0.5% as financials, materials and other cyclicals came under pressure. The S&P 500 finished up 1.3%, clawing back a sharp Tuesday selloff in semiconductors, while the Nasdaq Composite added 1.7%, buoyed by a rebound in chip names. Semiconductors were volatile, falling hard around Tuesday before recovering late in the week as South Korea's SK Hynix, the world's largest maker of high-bandwidth memory, prepared its Nasdaq debut. US small caps slipped -0.6% with the Russell 2000 hovering just below the 3,000 mark. Developed international stocks ended the week relatively unchanged and emerging markets recovered from last week's weakness with at 1.8% gain as Korea's KOSPI rebounded 4.6% and exited bear-market territory.

Fixed Income: Treasury yields took a leg higher as geopolitical risks intensified. The 10-Year Treasury yield rose 4.56% as renewed Middle East conflict and the release of June’s FOMC meeting minutes reinforced expectations that the Fed will stay higher for longer. Private credit news was mixed, with HSBC reportedly pulling back from lending to riskier direct-lending funds following a string of high-profile bankruptcies, even as BlackRock argued the sector will take on a still-larger role financing the AI infrastructure buildout.

Commodities: Oil prices surged early in the week as the US hit strikes on Iranian targets, with West Texas Intermediate rising as high as $76 a barrel and Brent Crude peaking at over $80 before the benchmarks retreated to around $71 and $76, respectively. Strait of Hormuz traffic slowed again amid the renewed hostilities, with most visible flows moving along Iran-approved routes.

WEEKLY ECONOMIC SUMMARY

Hawkish Fed Minutes: Minutes from Chairman Warsh's first meeting (June 16–17), released Wednesday, struck a firmly hawkish tone. The Committee voted unanimously to hold the funds rate at 3.50%–3.75% and dropped wording that had suggested an easing bias, judging risks to inflation as tilted to the upside. In keeping with Warsh's push for the Fed to communicate less about future intentions, the post-meeting statement ran about one-third of its usual length, and he again declined to submit his own rate projection. Separately, Chairman Kevin Warsh announced the leadership of five task forces to review the central bank's approach to key areas of policymaking. The response was generally positive as to the qualifications of the diverse group of appointees, which consists of business leaders, central bankers, and academics.

Iran Ceasefire Collapses: The interim US-Iran truce unraveled this week. Beyond the strikes and retaliation, de-escalation hopes resurfaced by Friday, with Trump saying Iran had called to make a deal through Qatari and Pakistani intermediaries. Former Supreme Leader Ayatollah Ali Khamenei's multiday state funeral concluded July 9, although his son and successor Mojtaba Khamenei remained out of the public eye.

Housing Weakness: June existing home sales unexpectedly fell 2.4% to a 4.09 million annualized pace, below the 4.2 million consensus, as the recent run-up in long-term rates weighed on activity. President Trump has taken a conflicting position on the housing market at times, wanting lower rates to spur homebuying but also wanting to preserve higher prices and home value wealth for Americans. Trump refused to sign the bi-partisan 21st Century ROAD to Housing Act, which softened several regulations and capped corporate home ownership, but the move was largely performative in protest to Congress’ inability to pass voter ID laws. The bill automatically became law over the weekend as Trump declined to veto it.

The week ahead: June CPI is due out Monday, while Chairman Warsh’s testimony to Congress will take place Tuesday and Wednesday. Second-quarter earnings season kicks off with several large U.S. financial institutions reporting beginning Tuesday.

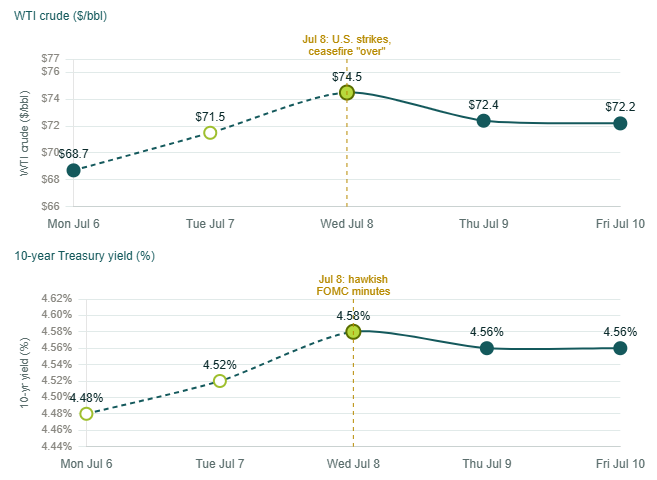

CHART OF THE DAY

The Chart of the Day shows the correlated move higher in both crude oil and interest rates as failed negotiations gave way to renewed hostilities in Iran, with both peaking Wednesday as President Trump pronounced negotiations to be over during his speech to NATO. While this wouldn’t be the first time negotiations ended only to later resume, this setback is notable because it came while the supposed Memorandum of Understanding was in place. While Wednesday’s Fed minutes also contributed, the deteriorating chances of a diplomatic resolution added to the pressure on interest rates.

Data Sources: Trading Economics. Commentary by VestGen Investment Management.