Markets Close First Half on Strong Note

WEEKLY MARKET SUMMARY

Global Equities: The first half of 2026 ended amid a holiday-shortened week, capping off a strong six months of performance despite a turbulent geopolitical landscape. The S&P 500 finished up 1.8%, its best week in two months, while the Nasdaq Composite added 2.1% despite semiconductors coming under renewed selling pressure. The Dow Jones Industrial Average was the standout, rising 2.0% to a record high close of 52,900, aided by strength in Apple (AAPL), Microsoft (MSFT), and traditional cyclicals. US small caps lagged during the week, with the Russell 2000 slipping back below the 3,000 mark and ending with a -0.8% pullback. Developed international stocks edged 1.8% higher while emerging markets were the weak spot, dragged down -2.2% for the week as Korea’s memory-heavy KOSPI suffered steep losses late in the week.

Fixed Income: Treasury yields backed up over the week, reversing the prior week’s flight to safety. The 10-Year Treasury yield finished at 4.49%, with the 2-Year at 4.14%, up from the roughly 4.38% level where the 10-Year had ended the previous week. Even so, the soft June jobs report on Thursday cut into near-term tightening bets: markets trimmed the odds of a July rate hike to about 18%, down from roughly 29% a week earlier. Fed Chairman Kevin Warsh, speaking at the ECB Forum, noted that inflation expectations had eased over the past month and there was no urgency to raise rates, while reiterating the central bank’s commitment to restoring price stability. He also repeated his view that the Fed’s balance sheet is too large and hampers policy transmission, keeping the door open to further runoff.

Commodities: Oil prices stabilized near pre-war levels after the prior week’s roughly -10% plunge, with West Texas Intermediate hovering near $69 a barrel and Brent trading in the $73 range. The tentative ceasefire held and Strait of Hormuz traffic continued its partial recovery with the United Arab Emirates reportedly restoring exports to over 3.9 million barrels per day.

WEEKLY ECONOMIC SUMMARY

June Jobs Data Disappoints: Nonfarm payrolls rose by just 57,000, well below consensus expectations, while the unemployment rate ticked down to 4.2%. Adding to the softness, prior months were revised lower, with May cut to 129,000 from 172,000 and April revised down to 148,000 from 179,000. Investors read the weakness as a silver lining, since it eases pressure on the Fed’s more hawkish members and lowers the odds of a near-term hike. Private Education and Healthcare were responsible for the entirety of the gains, adding 69,000 jobs, while Leisure and Hospitality was concerningly weak. The World Cup alone was anticipated to add 40,000 jobs, but the total for the sector came in at a loss of -61,000 during what should be a strong season for hotels and tourism.

Iran Update: Progress on negotiations was muddled by conflicting narratives over what concessions Iran will walk away with. Iran has insisted that “service fees” will be charged on vessels navigating the Strait of Hormuz as part of the terms for a lasting ceasefire, but the US has disputed that claim. Oman, which shares the strait, proposed a similar fee this week as well, despite being a neutral party to the conflict. Further negotiations were put on hold with Iran holding a multiday funeral for former Supreme Leader Khamenei through July 9th.

Factory Activity Cools: The ISM Manufacturing PMI slipped to 53.3 from 54.0 in June, just below the 53.8 forecast but still marking a sixth straight month of expansion. Encouragingly for the inflation outlook, the survey’s price components softened notably, with wholesale energy prices reported to have returned to levels seen before the Middle East conflict.

The week ahead: Minutes from Chairman Kevin Warsh’s first meeting as Fed Chair are the highlight of a relatively light week of economic data.

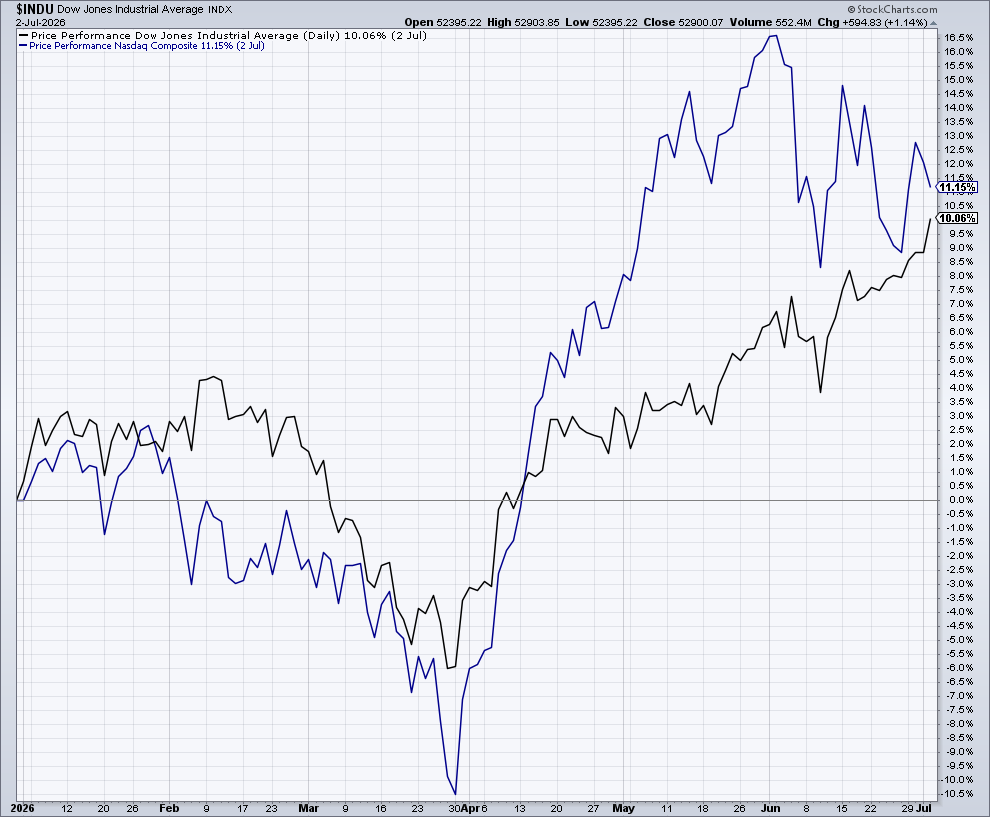

CHART OF THE DAY

The Chart of the Day shows the year-to-date performance of the Dow Jones Industrial Average (Black Line) and the Nasdaq Composite (Blue Line). The tech-heavy Nasdaq led the rally off the March lows, bolstered by euphoria over AI stocks. The index has sputtered, however, and consolidated in a wedge pattern since May, unable to break out to further highs. Meanwhile, the Dow Jones Industrial Average has been a stalwart and steady advancer, nearly catching up to the Nasdaq as tech fell out of favor and investors rotated back into old-fashioned, cyclical blue-chip stocks. While disappointing to tech investors, broadening of participation is generally seen as necessary for sustained market momentum and should be seen as a long term positive development.

Chart: Stockcharts.com.

Commentary by VestGen Investment Management.