Markets Rotate as Technology Stocks Retreat

WEEKLY MARKET SUMMARY

Global Equities: US equities slipped despite a relatively calmer geopolitical backdrop, as technology stocks came under selling pressure and investors rotated out of high growth names in advance of quarter-end rebalancing. The S&P 500 ended the weekly session -1.9% lower, while the Nasdaq pulled back -4.6% in its worst week since early April. The Dow Jones Industrial Average was a relative outperformer with a 0.6% weekly gain. US small cap stocks outperformed with the Russell 2000 registering a gain of 1.0% during the week. Developed international stocks slipped -1.8% while emerging markets suffered heavy losses as South Korean tech stocks sold off, dragging the MSCI Emerging Market index down -5.1%.

Fixed Income: The 10-Year Treasury yield tested the 4.5% mark early in the week, but slipped to 4.37% by week’s end, the lowest level since before the Iran war started. Rate hike odds for July rose, with markets pricing in a 30% likelihood the Fed will raise interest rates when it meets next month. Private Credit funds were back in the news as liquidity was tested from funds run by Apollo and Ares Management, prompting both companies to cap withdrawals.

Commodities: Oil prices fell by their largest margin in a month, with West Texas Intermediate prices sliding roughly 10% during the week and slipping below $70 a barrel at one point. The catalyst was an uptick in tanker traffic through the Strait of Hormuz, although that progress is at risk of being halted after Iran fired drones at a commercial ship on Thursday and the US retaliated with strikes right after markets closed for the week on Friday.

WEEKLY ECONOMIC SUMMARY

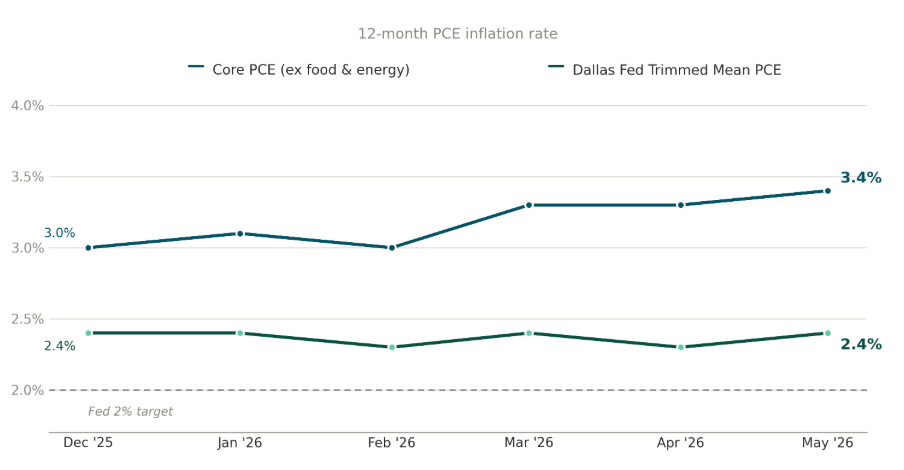

PCE Inflation: Investors shrugged off the latest data from the Fed’s preferred inflation measurement, the Core Personal Consumption Expenditures (PCE) index, which showed a 0.3% uptick in prices (ex-food and energy) for an annual rate of 3.4%. The headline reading reflected the impact of energy prices, up 0.4% monthly and 4.1% annually. Both readings were in line with expectations, and since PCE lags other measures such as CPI, the impact on markets was minimal. Investors are hoping that with the recent relief in oil prices, peak inflation may finally be in the rearview mirror. Trimmed Mean PCE, an alternative measure that new Fed Chairman Kevin Warsh has advocated for, paints an even more optimistic picture of inflation at just 2.4%.

Final GDP Reading Improves: The final reading on first quarter GDP surprised to the upside, rising from 1.6% to 2.1%. The underlying reason, however, was not an uptick in economic output. Rather, the improvement in GDP was almost entirely due to a sharp downward revision to import growth, which counts as a subtraction in the GDP calculation. Import growth fell from 21.1% to 11.8%, while consumer spending was revised downward from 1.4% to just 0.5%, the slowest pace since Q1 2022.

Iran Update: The ceasefire was tested as Iranian drones hit a shipping vessel in the Strait of Hormuz, prompting a Friday retaliatory strike from the US. Meanwhile, the US and Iran continued to offer contradictory interpretations of the Memorandum of Understanding. Among the disputed points were the control of the Strait, which Iran says it will charge fees to operate in despite US protestations, and the conditions upon which UN nuclear inspectors will be granted access in Iran. Iran stated the inspectors would only be permitted once all sanctions are lifted, something the US has argued against. President Trump is facing growing opposition to the conflict domestically as he seeks an additional $88 billion supplemental spending package to replenish munitions, with reports of a heated dispute emerging with senior Republican leaders angry over the concessions and costs of the war. Despite additional exchange of fire over the weekend, the US and Iran agreed to “stand down for now” and meet again for negotiations in Doha, Qatar this week.

CHART OF THE DAY

The Chart of the Day shows the Core Personal Consumption Expenditures Index, which is the Fed’s official inflation measurement, compared to the Dallas Fed’s Trimmed Mean PCE, a measure new Fed Chair Kevin Warsh favors. Both measures seek to remove volatile month-to-month price fluctuations and provide a more accurate representation of the direction of overall prices in the economy. While Core PCE simply removes food and energy because they are traditionally the most volatile, the Trimmed Mean PCE takes a new approach and ranks monthly price changes of 177 categories of goods and services, keeping on average 55 to 60 that represents the midpoint of the distribution curve. Examining this month’s underlying data, many of the expected food and energy items were removed from Trimmed Mean PCE, but it also excluded a 63% surge in Tax Preparation Services, a 54% increase in Jewelry, and a 45% jump in Air transportation, among many other categories. The result of the Trimmed Mean PCE approach is a much more stable interpretation of overall inflation, as the 2.4% rate is essentially flat over the last year. Whether the Fed fully embraces this alternative measure remains to be seen, but it will likely be included in the discussion at upcoming meetings.

Data: US Bureau of Economic Analysis, Dallas Federal Reserve.

Chart and commentary by VestGen Investment Management.